5

Kazakhstan’s Microfinance Sector Adds 44.3% in Assets: Emerging Markets Drive Growth

No comments · Posted by Alex Smirnov in Economy

Intro

Microfinance institutions in Kazakhstan enjoyed a banner year in terms of asset growth, according to a new report from the National Bank of Kazakhstan. The sector as a whole saw assets grow by 44.3%, thanks largely to rising demand from emerging markets. This is great news for the country’s small businesses and entrepreneurs, who are increasingly able to access the capital they need to grow and expand.

Growth During the Quarantine

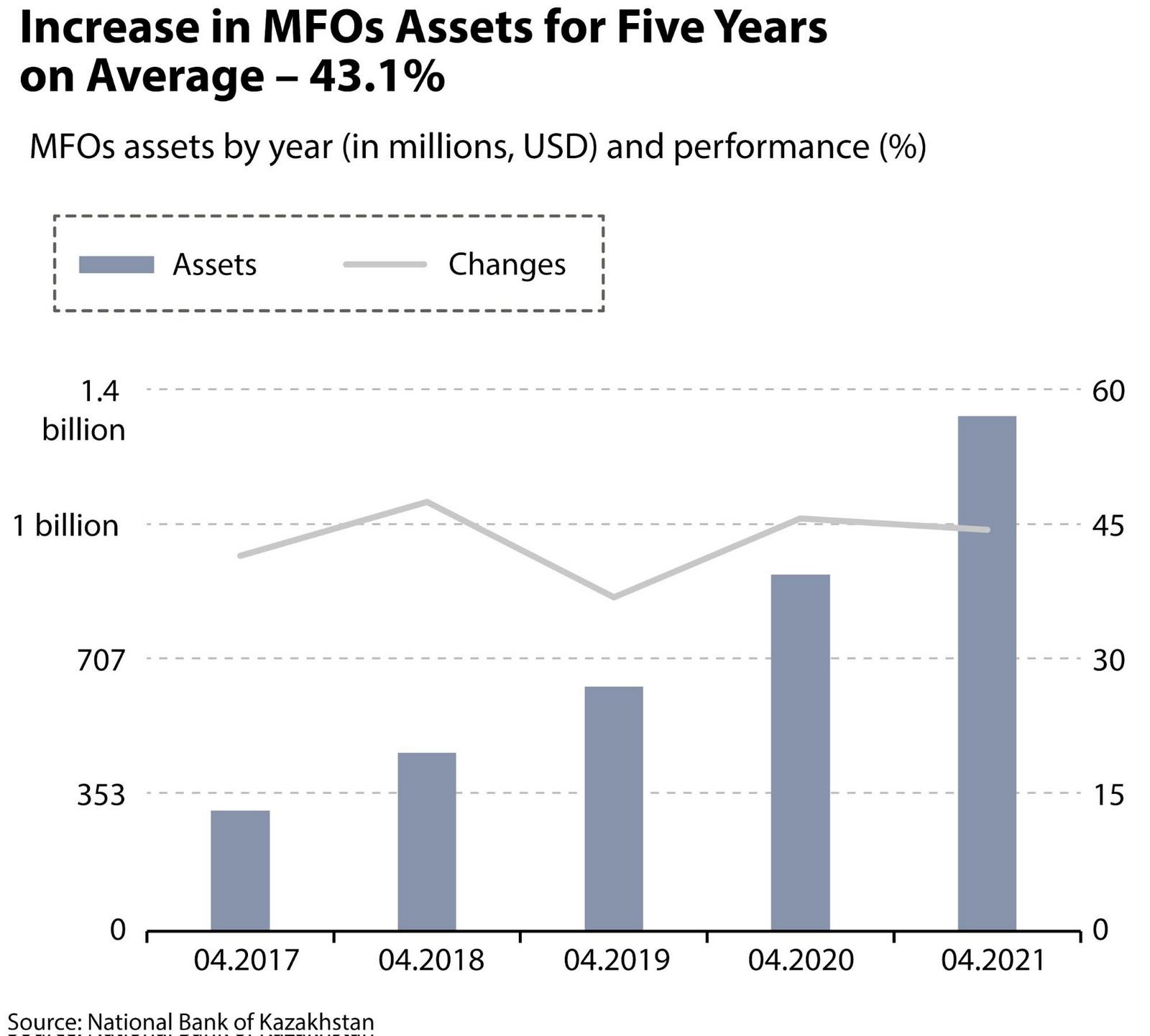

Kazakhstan’s microfinance sector has seen significant growth during the quarantine period. The number of microfinance organizations operating in the country has increased by 20%, and the average loan size has increased by 30%. The sector has also seen an increase in the number of new clients, with the majority of new clients being women. This growth is largely due to the fact that many Kazakhs have lost their jobs or had their income reduced due to the pandemic. As a result, microfinance organizations have been able to provide much-needed financial assistance to many families. The sector is expected to continue to grow in the coming months, as more and more Kazakhs turn to microfinance for financial assistance.

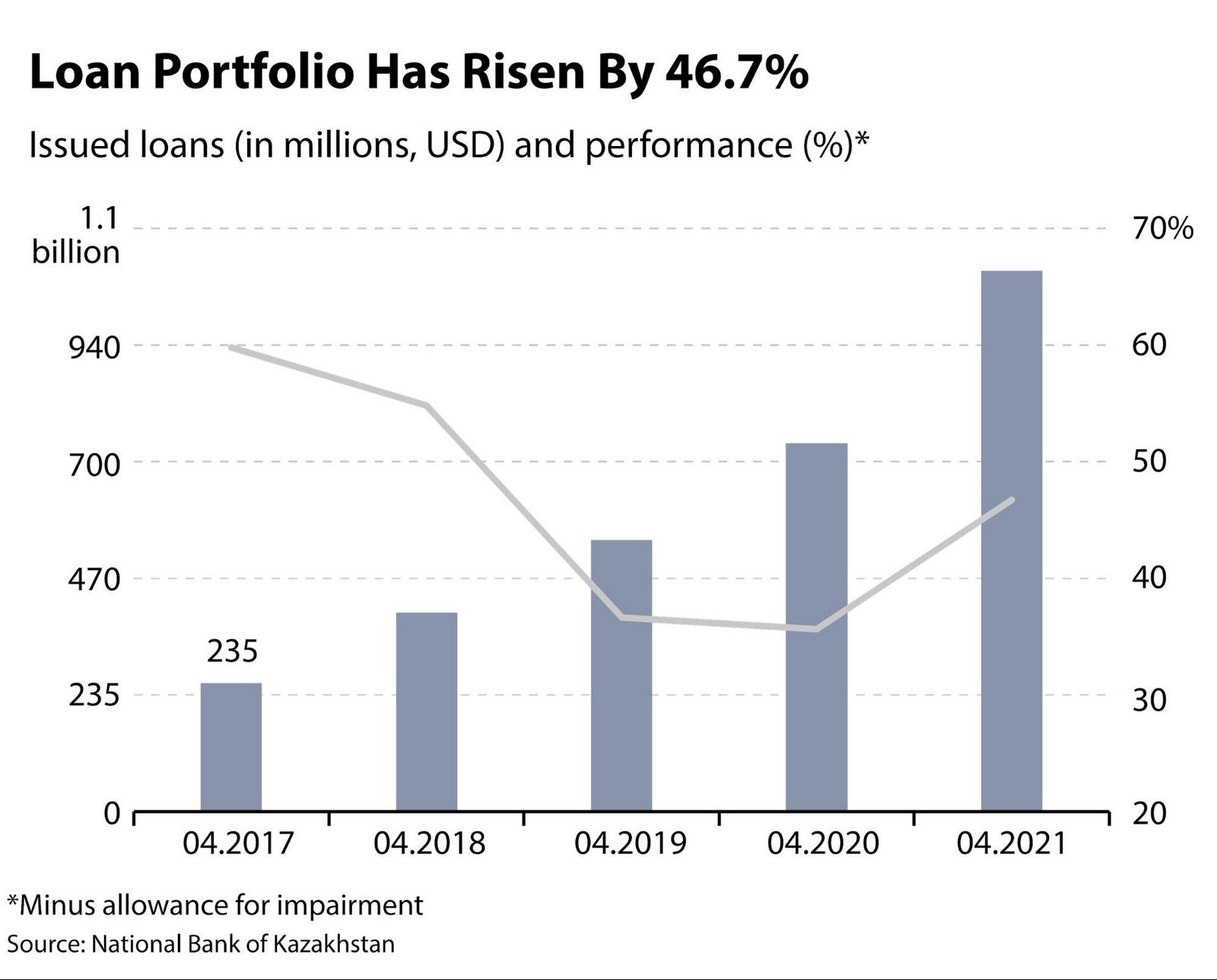

As of June 2019, there were a total of 220 MFOs operating in Kazakhstan, up from 199 in the previous year. These MFOs have seen their total assets rise to just over 1 trillion tenge (US$2.7 billion), according to the National Bank of Kazakhstan. This increase is due in part to the fact that more people are using MFOs for their financial needs. In addition, the average size of an MFO has also increased, as larger organizations have entered the market. The result is that MFOs are now playing a more important role in the Kazakhstani economy. They are providing vital services to both businesses and individuals, and their contribution is only expected to grow in the coming years.

Old Players and Two Newcomers

Two of the largest MFOs in Kazakhstan are AKSH and KAZKOMMERTSBANK. These two banks account for a significant portion of the country’s microfinance assets. Other large MFOs include Akshamat, Tsesna Bank, and Zaman-Bank. In addition to these old players, there are two new entrants to the market: Sberbank and VTB. Both of these banks are from Russia and have a strong presence in the Kazakhstani market.

The Future of Microfinance in Kazakhstan

Microfinance has become an increasingly popular means of providing financial services to underserved populations around the world. In Kazakhstan, microfinance institutions (MFIs) have been working to expand access to financial services and foster entrepreneurship among the country’s small business owners. However, the sector faces a number of challenges, including high interest rates and a lack of regulation.

ROA and ROE

ROA and ROE – two of the most important indicators. When it comes to profitability, MFOs in Kazakhstan are doing quite well. The average ROA (return on assets) for Kazakhstani MFOs is 12.42%, while the average ROE (return on equity) is 19.73%. These numbers are significantly higher than the global averages of around 11% and 15%, respectively. This indicates that microfinance is a very profitable business in Kazakhstan.

Interest Rates

One of the main challenges facing the microfinance sector in Kazakhstan is high interest rates. The average interest rate on loans from MFIs is 28.17%. This is significantly higher than the global average of 20%. In addition, the rates charged by some MFIs can be as high as 60%. The high interest rates make it difficult for borrowers to repay their loans, and they also make microfinance less affordable for potential borrowers.

Increased Regulation of Microfinance Institutions

In response to increasing the number of microfinance institutions, the government has proposed new regulations that would require MFIs to obtain a license from the central bank. The proposed regulations would also put limits on the interest rates that MFIs can charge, and would impose other requirements designed to protect consumers.

The government argues that these regulations are necessary in order to safeguard consumers and prevent predatory lending practices. However, some observers have raised concerns that the regulations could stifle innovation and discourage MFIs from operating in Kazakhstan. It remains to be seen how the proposed regulations will ultimately be implemented, but it is clear that the landscape of the microfinance sector in Kazakhstan is changing.

Conclusion

Despite these challenges, the future of microfinance in Kazakhstan is promising. The government has expressed commitment to supporting the sector, and a number of initiatives are being implemented to improve the regulatory environment. In addition, MFIs are innovating and developing new products and services that meet the needs of their clients. With continued support from the government and the private sector, microfinance in Kazakhstan will continue to grow and play a vital role in inclusive economic development.

Tags: No tags